Startup Business Loans: A Guide for Entrepreneurs

Starting a business comes with many challenges, and one of the most significant hurdles for new entrepreneurs is securing funding. Whether you’re looking to launch your startup or expand an existing business, startup business loans can provide the financial boost you need. In this article, we will explore various types of startup business loans, how to qualify, and how to use them effectively to set your business on a path to success.

What Are Startup Business Loans?

Startup business loans are financial products designed to help entrepreneurs and new business owners obtain the capital needed to launch or grow their businesses. Unlike traditional business loans, these loans are typically offered to businesses that may not yet have a proven track record of profitability or extensive credit history. The purpose of a startup business loan is to help cover initial expenses such as equipment, inventory, marketing, hiring employees, and other startup costs.

These loans can be obtained from a variety of lenders, including banks, online lenders, and even government-backed programs. Since many startups are riskier ventures, the terms and approval criteria for these loans may vary depending on the lender and the specific loan type.

Types of Startup Business Loans

There are several types of startup business loans, each with its own set of requirements and benefits. Understanding the different options can help you make an informed decision about which type of loan is best for your startup.

Government-Backed Loans

One of the most popular forms of startup business loans are government-backed loans, particularly those offered by the Small Business Administration (SBA). These loans are designed to help small businesses that may not qualify for traditional loans. SBA loans offer favorable terms, including low-interest rates and longer repayment periods.

Eligibility for SBA loans depends on factors like the size of your business, the industry you operate in, and whether your business is for-profit. While SBA loans may take longer to process, they are a reliable option for many startups.

Bank Loans

Traditional bank loans are another common financing option for startups. These loans typically have more stringent approval requirements, including a solid credit history, a proven business model, and financial projections. While the application process may be more challenging, bank loans can offer larger sums of capital and competitive interest rates.

Microloans

If you’re looking for a smaller loan or if your business is in its very early stages, microloans can be an excellent choice. Microloans are generally easier to qualify for than traditional loans, and they are ideal for businesses that need less capital to get started. These loans are typically offered by non-profit organizations or online lenders and come with relatively low-interest rates.

Online Lenders

Online lenders are increasingly popular among entrepreneurs due to their speed and convenience. Many online lenders offer startup business loans with minimal paperwork and faster approval times than traditional banks. These loans are often unsecured, meaning you don’t need to provide collateral, but they may come with higher interest rates.

Online lenders are a great option for entrepreneurs who need quick access to funding or who may not qualify for a traditional loan.

Grants and Special Programs

Some startups may be eligible for grants or special loan programs that don’t require repayment. These programs are often offered by government agencies, nonprofit organizations, or private companies, and are designed to support specific industries or business types. While these opportunities can be highly competitive, they are worth exploring for startups that meet the criteria.

How to Qualify for a Startup Business Loan

Qualifying for a startup business loan depends on several factors. While requirements can vary by lender, there are some key elements that most lenders will consider:

Business Plan

A well-thought-out business plan is one of the most important documents you can present to a lender. A strong business plan should clearly outline your business goals, target market, competitive analysis, marketing strategies, and financial projections. This document demonstrates that you have a clear vision for your startup and a strategy for success.

Financial Projections and Collateral

Lenders want to see that your business will be able to repay the loan, so providing accurate financial projections is essential. Startups may also be asked to provide collateral to secure the loan, such as business assets or personal guarantees.

Credit Score

While startup businesses often don’t have a credit history, personal credit scores may be used to assess your reliability as a borrower. A higher credit score can increase your chances of loan approval and may help you secure better loan terms.

Demonstrating Potential

Lenders want to see that your startup has growth potential. Highlighting your previous experience, industry knowledge, and any early success or traction can help demonstrate that your business has the potential to succeed.

Top Lenders for Startup Business Loans

When it comes to startup business loans, the right lender can make all the difference. Here are some of the top lenders for startup loans:

- SBA Lenders: For businesses that qualify for SBA-backed loans, these lenders offer competitive interest rates and favorable terms.

- Traditional Banks: Banks like Chase, Wells Fargo, and Bank of America offer startup loans to businesses with a solid business plan and good credit.

- Online Lenders: Lenders like OnDeck, Kabbage, and Fundera provide quick and easy access to startup funding with fewer requirements.

- Community Development Financial Institutions (CDFIs): These lenders focus on helping underserved communities and often offer microloans with more flexible terms.

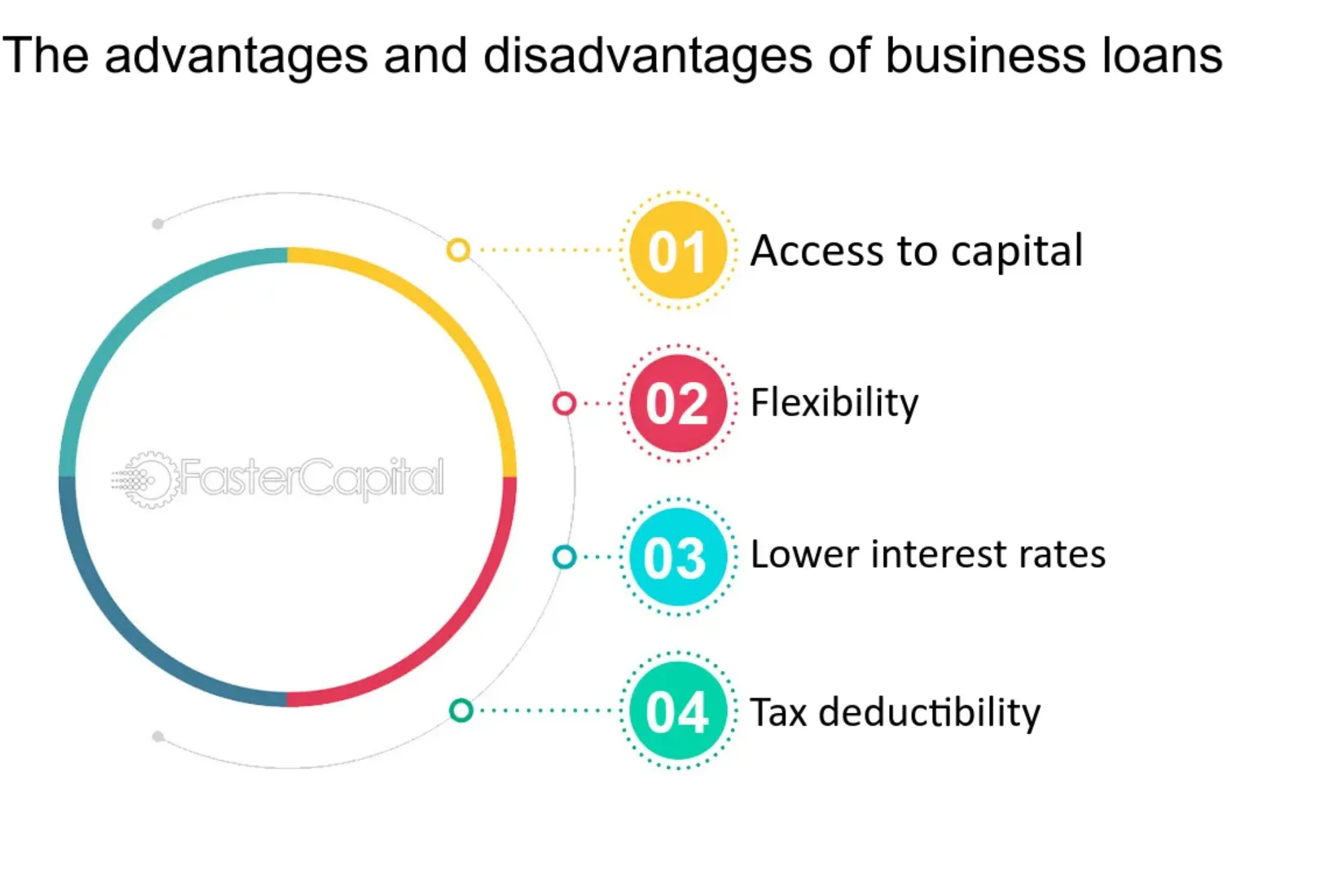

Pros and Cons of Startup Business Loans

While startup business loans can be a valuable tool for funding your business, it’s important to weigh the pros and cons before moving forward.

Advantages

- Access to Capital: Loans provide the necessary funds to help you start or grow your business.

- Tax Benefits: Interest paid on business loans is often tax-deductible.

- Build Credit: Successfully repaying a loan can help establish or improve your business credit.

Disadvantages

- Debt Repayment: Loan repayment is a financial commitment that must be managed carefully.

- Risk of Denial: Not all startup businesses will qualify for loans, particularly if you lack a strong credit history.

- High Interest Rates: Some loan types, particularly online loans, come with higher interest rates, which can be a significant financial burden.

Alternatives to Startup Business Loans

If securing a startup business loan doesn’t seem like the right option, there are several alternatives to consider:

- Bootstrapping: Using your own savings to fund your startup is a risk-free option, but it can limit your capital.

- Crowdfunding: Platforms like Kickstarter or GoFundMe can help you raise funds from a large number of small investors.

- Angel Investors and Venture Capital: These investors provide capital in exchange for equity in your business.

- Business Incubators and Accelerators: These programs offer financial support, mentoring, and resources to help startups grow.

Tips for Managing Loan Funds Effectively

Once you’ve secured a startup business loan, it’s essential to use the funds wisely. Here are a few tips for managing your loan funds effectively:

- Create a Budget: Plan your expenses carefully and allocate funds for specific purposes like marketing, equipment, or hiring.

- Track Expenses: Keep detailed records of all expenditures to ensure you’re staying on budget and managing your loan efficiently.

- Focus on Cash Flow: Ensure your business generates enough revenue to cover loan repayments and operating costs.

FAQs on Startup Business Loans

Can I get a loan with no credit history?

It may be challenging to secure a loan without any credit history, but some lenders, especially online lenders or microloan programs, may offer options for startups with little to no credit.

What documents are typically required?

Common documents include a business plan, financial projections, tax returns, and any relevant personal financial information.

How long does the application process take?

The application process can vary depending on the lender, but online lenders often provide faster approval than traditional banks, sometimes within a few days.

Startup business loans can provide the financial support you need to bring your entrepreneurial dreams to life. Whether you choose a government-backed loan, a traditional bank loan, or an alternative financing option, it’s essential to understand your options and qualifications. With the right loan and financial management, your startup can thrive and grow.

Call to Action: Ready to explore startup business loans for your venture? Research the best options, and don’t hesitate to consult with a financial advisor to guide you through the process.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}